Part 2b: Betterhelp's First Test

Mental Health's Supercycle · Part 2b. Betterhelp Q1 2026 results just dropped. Revising valuation upwards Beyond Billions · May 2026

Six weeks ago I wrote that the April earnings call was the first real test. The numbers are in.

Insurance Business: Crushing it. 🎉

In April 2025, Betterhelp acquired UpLift, getting over 100 million lives with a network of about 1,500 clinicians. In Q3 2025, five months post-acquisition, BetterHelp was live in only 7 states and DC. By Q1 2026, just two quarters later, they are in 30 states with over 6,000 credentialed providers and 150 million contracted lives. This is incredible progress and sets them up for success.

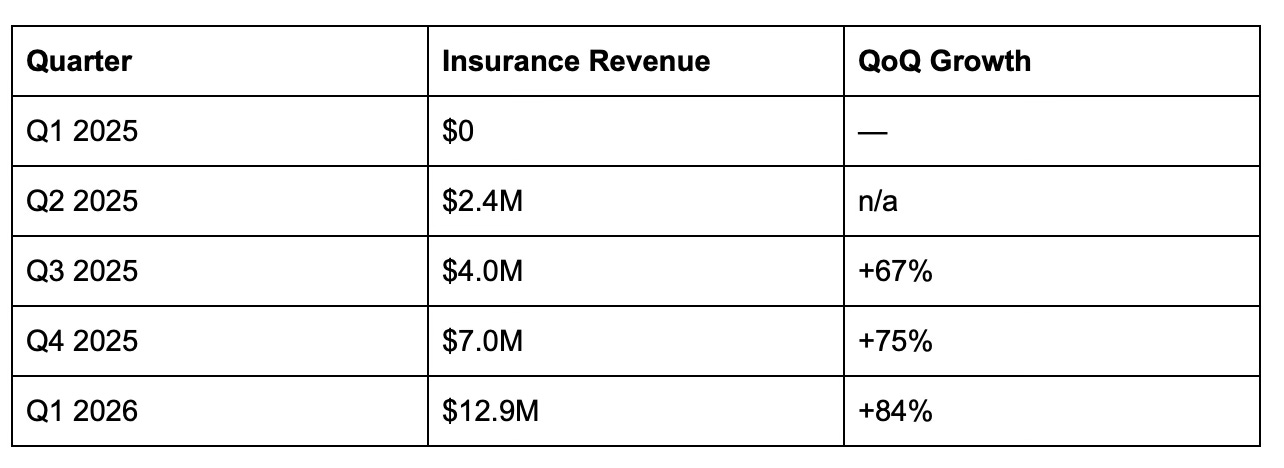

For revenue, we modelled $75M base case, $90M bull case for full-year 2026. Q1 came in at $12.9M. Management then raised full-year guidance to $90-105M and said they expect to exit 2026 at an annualised run rate above $125M. That’s slightly above our bull case that modelled $90M for 2026. But does the guidance seem credible.

Here’s the full picture quarter by quarter:

QoQ growth is accelerating. The absolute jumps are getting larger each quarter. One important note: 2025 insurance revenue was largely Uplift’s existing payer contracts, not organic BetterHelp growth. Q1 2026 is the first quarter where BetterHelp’s own nationwide rollout is the primary driver. If credentialing and contracting lands on schedule, the H2 ramp is plausible. If it slips, the guidance doesn’t hold.

Watch Q2. If insurance revenue hits $20M+, guidance is credible.

DTC decline: Base case, on track. ✅

We said BetterHelp was a supertanker. $937M of DTC revenue that had to be tapered, not killed. We modelled 15% annual decline. Q1 DTC fell 14% year-over-year. Management cut ad spend by $16.7M, rationing the decline deliberately. The gentle steer is exactly what’s happening.

Margin compression during transition: Called it. ✅

We wrote about “the pivot inside the pivot”, that the cultural transformation would be expensive before it got better. BetterHelp EBITDA margin collapsed from 3.2% to 0.9% in Q1. A 75% drop.

Blue Orca liability: Unresolved. ⚠️

No regulatory action as of Q1. No disclosure of actual incentive structures. Hasn’t crystallised, hasn’t cleared. Still a structuring question for any buyer.

PE buyout: Thesis intact, valuation revised up. 🕐

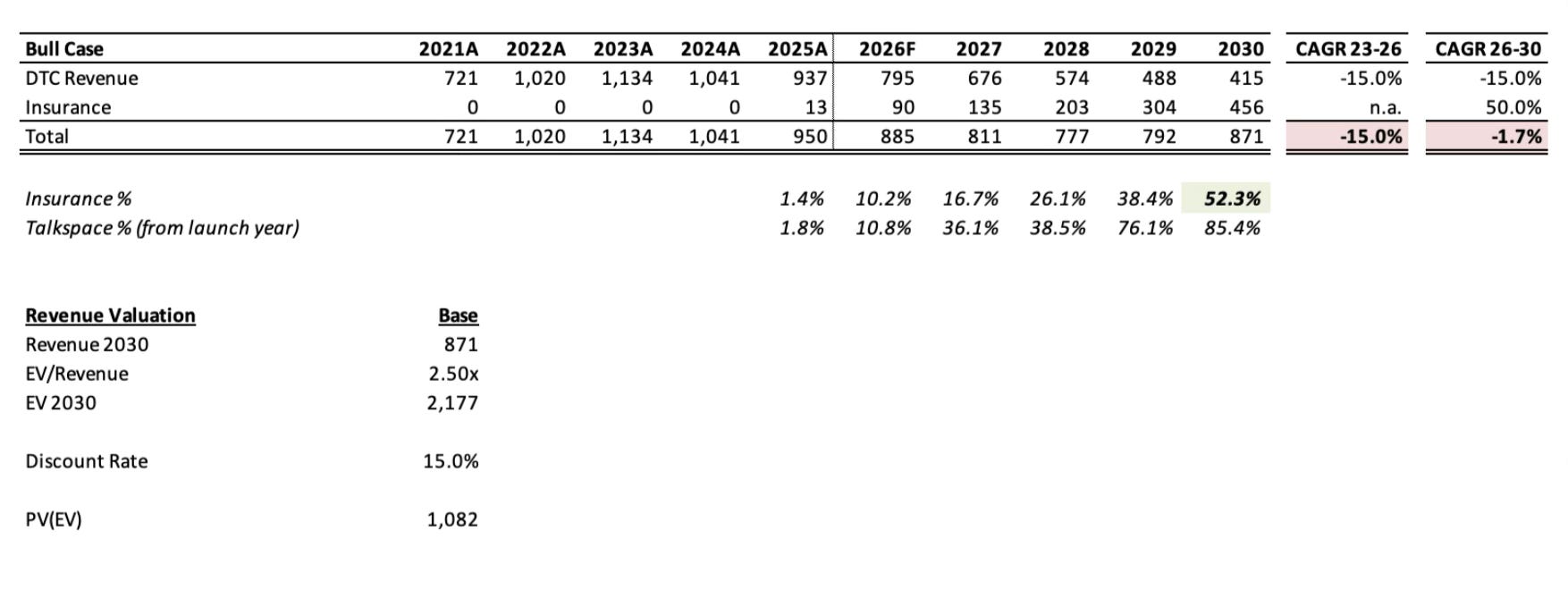

The case for a PE investor to submit a bid is now stronger, as the pivot visibility is clearer. We revise our underwriting to $90M insurance revenue for 2026 and 50% CAGR going forward, which is the pace of Talkspace’s pivot. We keep our assumption of -15% CAGR for DTC intact.

Valuation on a revenue basis is now ~$1.1B. On EBITDA basis it’s below $1B. A private equity house would likely still open with $950M, but would now be willing to move upwards towards $1.1B. At that valuation they can still make north of 3x in 4 years, a solid return for PE.

Betterhelp management is starting to establish execution credibility. PE should be willing to pay more to carve Betterhelp out, as the pivot is more bankable. But management is more likely to dig their heels, arguing they will get much more value in 3-4 years time. Every quarter of solid execution increases PE willingness to pay and reduces likelihood of the board approving a deal.

Saki is the founder of Evio, building the leading mental health investment platform.

Beyond Billions documents the build, in public.

Mental Health’s Supercycle documents Evio’s investment thesis.