Part 2a: Let's Buy BetterHelp

Mental Health's Supercycle · Part 2 of 4. The behavioral health sector is entering a supercycle · In four articles I am writing about why, how and what Evio is doing about it.

In Part 1, we covered Talkspace: a company that nearly died clinging to a DTC cash-pay model, then sold for $835 million after a brutal pivot toward payers. The lesson is clear: the market tailwinds are here, but you have to build the right business model to benefit. Quality management is paramount. Jon Cohen was the right person for the job and he turned the ship around.

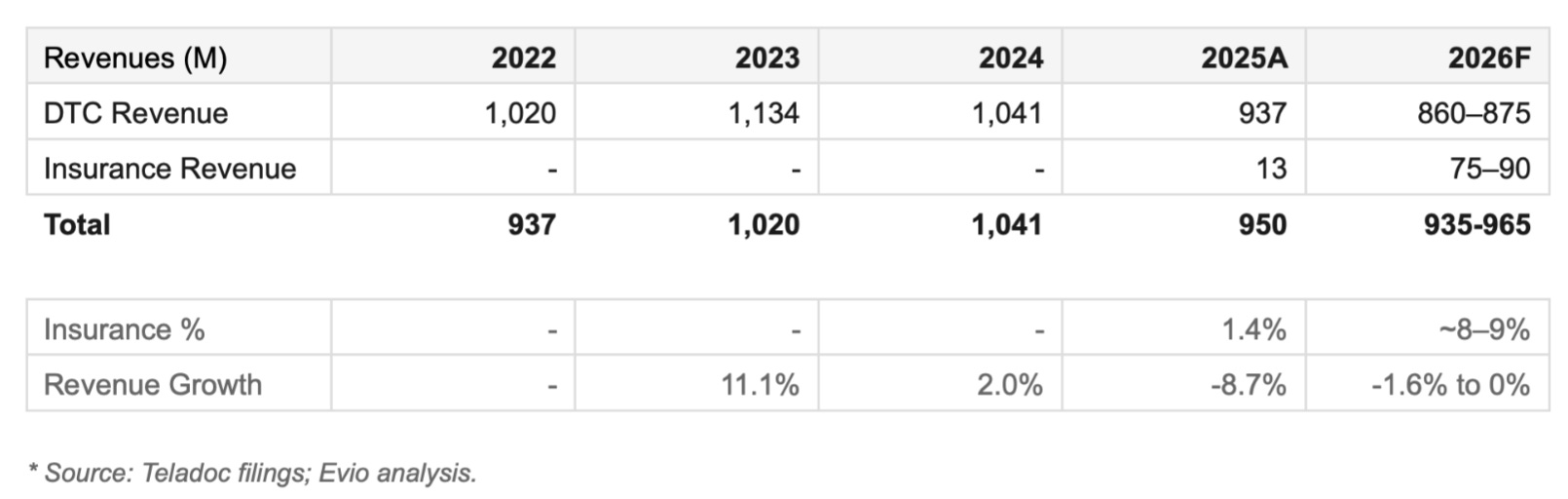

BetterHelp is a very different story. The company thrived as a DTC cash-pay business within Teladoc during and post-COVID, reaching $1.1 billion in revenue. But as of 2025, insurance revenue was still under 2% of the mix. The DTC engine is now in structural decline.

The more interesting story is Teladoc itself. The whole company trades at an enterprise value of roughly $1.2B today, against a peak of $47B. EBITDA multiple is 4.4x, a distressed valuation versus comparables.

We do a Sum Of The Parts that shows that Betterhelp’s components are independently worth $3.6B. The market’s valuation of Teladoc of $1.2B points to several structural issues: how the businesses fit together, regulatory liability and lack of confidence in the management team.

In what follows we will work through the context that has led to this extreme market dislocation, decide how much Betterhelp is worth today and discuss why the board would struggle to say no to a carve-out bid.

The $4.5 million bet that became a $3 billion business

In January 2015, Teladoc acquired BetterHelp for $4.5M. What followed is one of digital health’s most remarkable value-creation stories. Fueled by COVID demand and aggressive paid social, revenue peaked at $1.1B in 2023, implying roughly $3B in EV assuming a multiple of ~2.5x. About 667x the purchase price.

The model was elegant: consumer subscription, $60 to $100 per week, no insurance required. It captured a generation of therapy-seekers who would never have navigated the traditional mental health system. And then the tailwind reversed.

The unraveling

For its first twelve years, BetterHelp accepted no insurance. Without payer relationships it was invisible to the infrastructure that routes most Americans into mental health care. When COVID demand normalised and CACs rose, there was no reimbursement floor to slow the fall.

Teladoc began the payer pivot seriously in April 2025 when it acquired Uplift for $30 million upfront and up to $45 million including earnouts. Uplift had $15 million in 2024 revenue, 1,500 credentialed clinicians, and payer contracts covering 100 million lives. The strategic logic was straightforward: BetterHelp had the brand and the user base but no payer infrastructure. Uplift had the payer infrastructure but no scale. The acquisition was Teladoc buying the credentialing and contracting rails it needed to route BetterHelp users toward their insurance benefits rather than cash-pay subscriptions.

Insurance revenue for all of 2025 was $13M on a $950M total revenue base. Under 1.4%. The 2026 guidance calls for $75 to $90 million, a 6x to 7x increase in a single year. Hit these numbers and the market will buy that the pivot is underway. Still, it comes almost a decade late. And it is happening inside a corporate structure that is the wrong home for it.

The marriage that never made sense

When Teladoc merged with Livongo in 2020 for $18.5B, the pitch was integration: one platform spanning physical and mental health, chronic condition management, and behavioral support. None of it materialised.

BetterHelp remained a standalone consumer subscription business. No shared clinicians, no shared payer contracts, no shared data. Worse, Integrated Care, Teladoc’s B2B segment, was selling mental health services to the same employers and health plans that BetterHelp was trying to reach. The left hand didn’t just fail to know what the right hand was doing. It was undercutting it.

A whale of a problem

In February 2025, Blue Orca alleged that BetterHelp therapists were using ChatGPT to generate responses, driven by word-count bonuses and caseloads of 40 to 60 patients. Teladoc denied it, but didn’t disclose what the actual incentive structures are. No regulatory action has followed as of March 2026. The short report was published eight days before the Q4 2024 earnings call. Neither management nor analysts raised it. That silence is its own signal. For a strategic buyer this is a deal breaker.

But a financial buyer would treat this as a liability with a defined cost. Structure the deal with a $150-200M escrow held for 24 to 36 months, released contingent on no material regulatory action. The liability becomes a negotiating point, not a deal breaker.

The pivot inside the pivot

Changing a revenue mix is a financial problem. Changing the machine that generates it is a cultural one. These are not the same problem, and confusing them is where most turnarounds fail.

BetterHelp was built around one organizing principle: acquire consumers cheaply and retain them profitably. Incentive structures, hiring profiles, therapist compensation, performance metrics, were all architected to serve that principle. CAC and LTV were the North Star. The therapist was a supply-side input optimized for throughput.

Insurance is a different business with a different logic. The customer is a payer, not a consumer. The sales cycle is much longer. The metrics that matter are utilization rates, outcomes data, and network adequacy, not subscriber counts and churn.

The Blue Orca report made this tension visible. Whether or not the AI allegations were true, the incentive structure they described, word-count bonuses, caseloads of 40 to 60 patients, is structurally incompatible with the clinical documentation standards that payers require. Restructuring clinician incentives across tens of thousands of therapists is not a policy update. It is a renegotiation of every implicit contract on the platform. Some will leave. Patient continuity will fracture. And it has to happen while DTC is still funding the transition.

The financial model can show a path to 40%-50% insurance mix by 2030. The harder question is whether the organization executing that model today is built to get there. The pivot inside the pivot is the hardest part of this business case. And there’s only one type of buyer that can deal with such transformation: an operationally competent PE firm, with experience in turnarounds.

The Talkspace mirror

Talkspace is the only clean transaction comparable. UHS paid $835M, or 3.65x revenue, for a business growing at 22% per year with 75% insurance mix and a 7% EBITDA margin at exit. That is a fundamentally different risk profile from BetterHelp today.

Size matters a lot in this case. At peak Betterhelp was ~10x larger in revenue. Being small and nimble, Talkspace was able to put the “melting icecube” that was DTC into the microwave, while ramping insurance very rapidly. Today they have only $21.5M in DTC, which is 10% of their revenue base.

By comparison Betterhelp is a supertanker that will be hard to pivot. A fast taper of DTC ads could be detrimental. There is $937M of DTC revenue at risk and you can’t credential and ramp clinicians fast enough to replace it. This has to be a gentle steer, rather than a hard pivot.

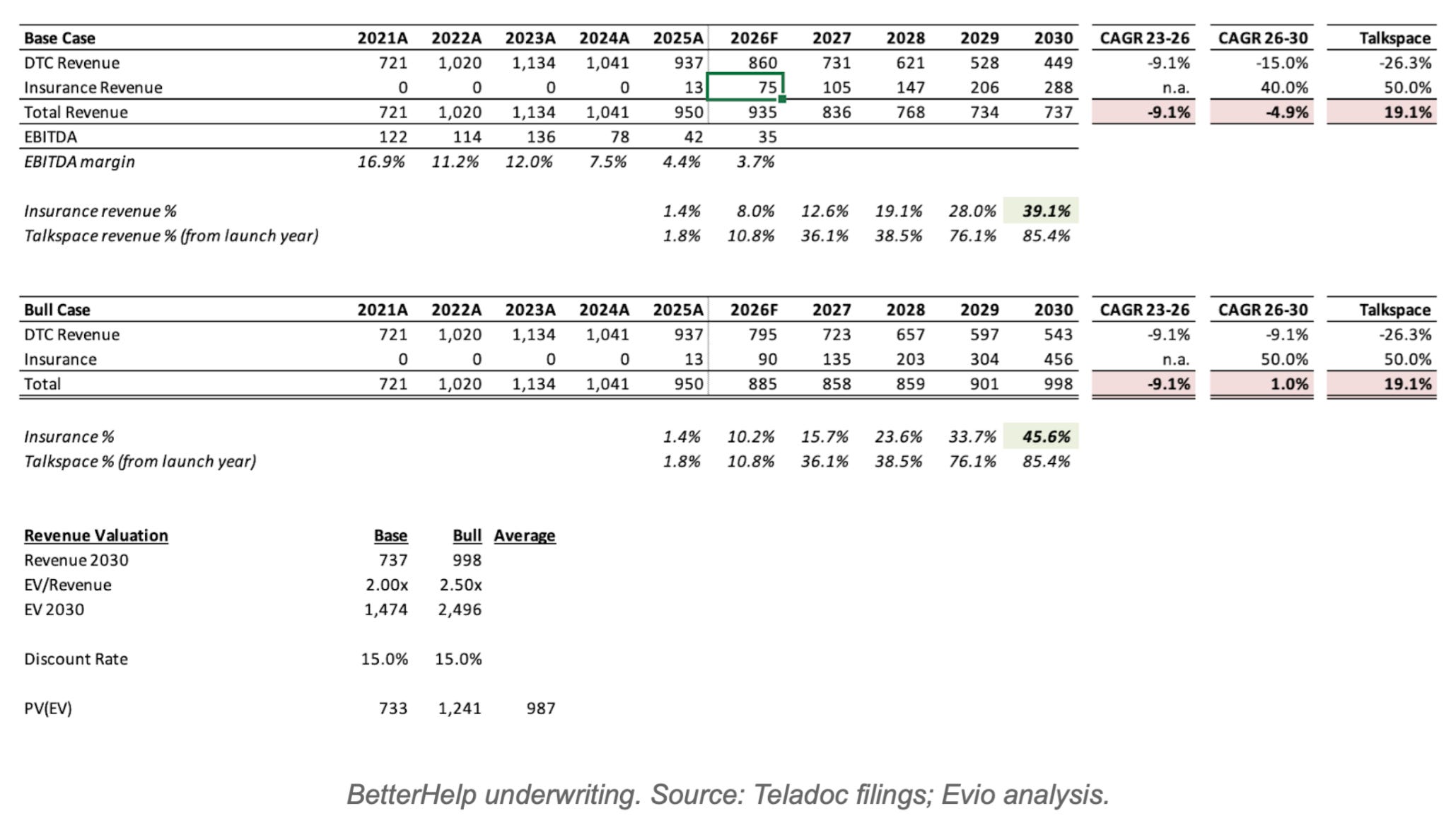

As such we cannot use the Talkspace ramp in insurance mix as a guide. In our base case we assume:

DTC decline accelerates to 15% per annum versus 26% in the Talkspace case.

2026 insurance revenues hit the lower end management forecast of $75M, up from $13M

Insurance growth is 40% per annum, lower than Talkspace’s 50%

By 2030 this leads to a 39% insurance mix and a revenue base that is declining by 5% per annum.

Our bull case we assume:

2026 insurance revenues hit upper end of management forecast of $90M

Insurance grows at 50%, the same growth rate as Talkspace

DTC will decline at the same pace it has been since 2023, 9.1%

This yields 46% insurance mix and a total revenue base that is growing at 1%.

Neither scenario resembles Talkspace at exit. Talkspace was growing at 19%. BetterHelp will still be shrinking or flat. The exit multiple will reflect that. We model the exit at 2.0x revenue in the bear case and 2.5x in the bull.

This leads to 2030 EV of ~$1.5B-2.5B. What we are willing to pay today depends on the discount rate that you apply. The best way to think of this is: what will the key shareholders expect as an annual return to stay invested in the face of a liquidity option. Public market investors generally seek about 10%. In this case there are idiosyncratic risks: the potential regulatory liability and questions about whether current management can complete this pivot within this current structure given incentives misalignment. I would expect investors would be targeting a minimum of 15% discount rate.

The market is right

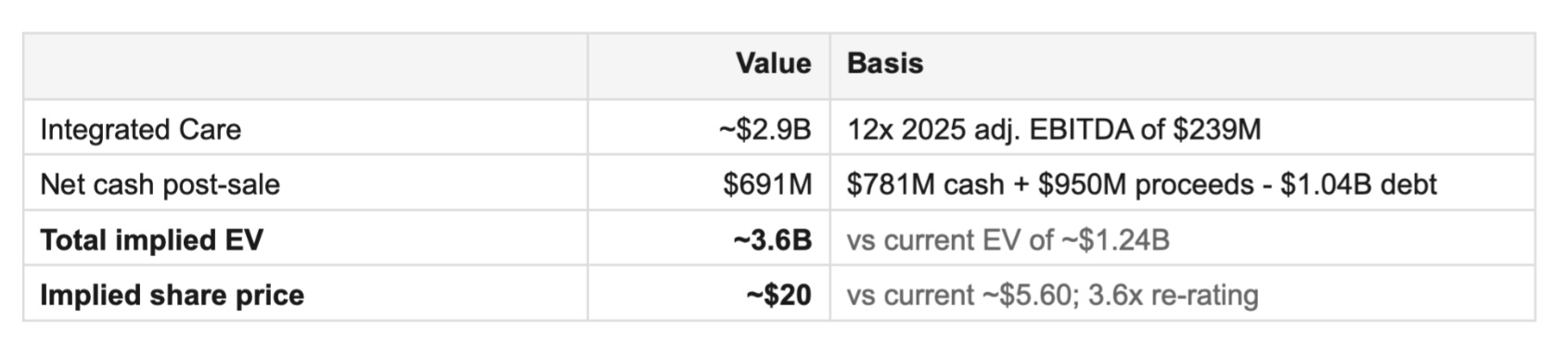

Before founding Evio I spent 15 years in and around private equity. I worked for a fund of funds looking at hundreds of co-investments every year alongside some of the best PE groups in the world. Based on that experience, and assuming the upcoming earnings call supports the 2026 forecast, I would pay up to $950M for BetterHelp, 1x revenue.

With that valuation, The Sum Of the Parts math is stark. Standalone Integrated Care at 12x EBITDA is worth roughly $2.9B. Net cash post-sale is roughly $691M. Total implied EV of $3.6B. The stock trades at $1.2B today. That’s a 66% discount!

It’s easy to think that the markets are mispricing this business. But the market is right in this case. It is saying that it does not believe the two businesses belong together, does not trust the management team to execute the pivot and cannot price the Blue Orca liability. A clean separation addresses all three.

The re-rating math implies roughly $20 per share against a current price of $5.60. A 3.6x return for doing nothing except separating two businesses that should never have been combined.

Who buys it and why

The right buyer is private equity, not a strategic. Only PE can deal with the complexity of the liability plus the execution risks of the pivot. PE takes it private, removes quarterly earnings pressure, and completes the pivot on a single mandate with properly aligned incentives.

Beyond the pivot playbook, what’s really interesting under PE ownership are bolt-on acquisitions. BetterHelp as a platform acquirer in a fragmented outpatient mental health market is a compelling thesis that no public company structure can execute cleanly. Cerebral has already shown the template: it acquired Inflow, a behavioral health app for individuals with ADHD and before that Resilience Labs, a clinician development platform. Small, strategic, capability-building acquisitions that a distracted public company cannot pursue. A PE-owned BetterHelp could run the same playbook at ten times the scale, buying credentialed regional practices, plugging them into the payer contracts being built, and assembling a hybrid virtual and in-person behavioral health platform that neither LifeStance nor Acadia can match on the consumer side.

The exit story then writes itself. By 2030 you have a scaled, profitable platform with 50% insurance mix, bolt-on acquisitions that demonstrate the model, and a consumer brand no competitor can replicate. That is a business that commands a genuine strategic premium from exactly the buyers who were the wrong acquirers in 2026.

Can a deal happen?

The Board dynamics will not be easy. Management will assert they can execute on the bull case, or even better, and deliver the value in 4-5 years time. But a credible $950M offer forces a formal fairness process. The Sum Of the Parts math is damning.

Institutional shareholders own 75% of the company and have watched the stock fall 98% from peak. The sell-now math is a letter that writes itself for any activist that builds a 5% position. And if Q1 or Q2 insurance revenue tracks below the $75 to $90 million full-year guidance, the internal transformation narrative collapses entirely. We’ll get a first read in the April earnings call.

The first test

The market will be watching 2026 insurance numbers closely. The April earnings call is the first real test. If insurance revenue tracks toward the $75-90M guidance, the $950M valuation holds. If it misses, the number moves materially lower.

Either way, this business belongs in private equity hands. Their job won’t be easy. But they stand to make 3x-5x on a clean execution. In a market starved for large-scale behavioral health platforms, that’s the deal of the decade.

Next in the series: Part 3 will cover the broader consolidation wave in behavioral health and what it means for independent platforms.

Saki is the founder of Evio, building the leading mental health investment platform.

Beyond Billions documents the building in public.

Mental Health’s Supercycle is a 4-part series that documents Evio’s investment thesis.